s110 MVLs

Section 110 reconstructions: A complicated corner of solvent liquidations

Frettens’ resident Insolvency Guru, Malcolm Niekirk, delivered one of his popular monthly coffee break briefings to insolvency professionals on Monday 10th May.

He spoke about section 110 reconstructions, what they are used for, what a typical transaction looks like and, each party’s role and timescales, as well as pricing the work.

Below, we have provided a summary of what was included. You can also download the slides and a recording of the presentation.

What is section 110?

Section 110 of the Insolvency Act, 1986, allows for a liquidator to accept shares (issued by a buyer) in consideration for assets transferred from a solvent company. The liquidator passes those shares to the shareholders. By that means, they become the owners of the company that now owns the business.

What is section 110 used for?

Most commonly, s110 is used to split a company that owns two businesses into two companies, each owning one business. This might happen if a family business has been passed down the generations and evolved into two distinct divisions.

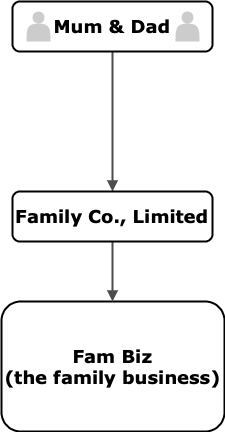

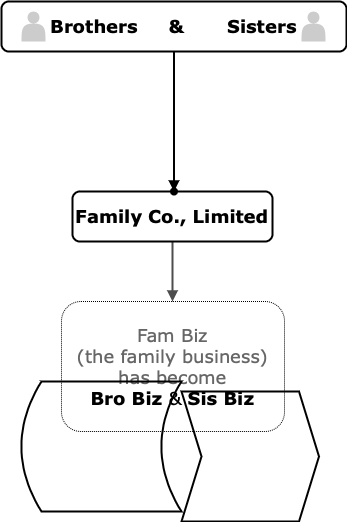

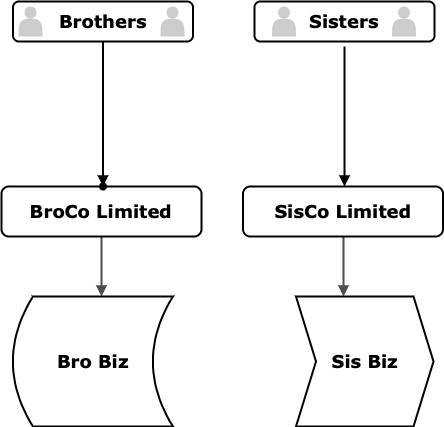

A typical s110 transaction

This might be what the business looked like a couple of decades ago.

This might be what it looks like now. The founders are enjoying their retirement. The business is in safe hands, and flourishing well, in the hands of the next generation. But it looks quite different from what it was originally. The two new elements no longer make business sense in the same company.

By using a s110 reconstruction, the businesses can be separated, and each put into its own company. Each company is owned by the family members most interested in that sector of the business. This is a tax efficient way of doing it, and usually will not trigger tax liabilities, despite the changes of ownership of companies and businesses.

Click here to read the full article.